All Categories

Featured

Table of Contents

[/image][=video]

[/video]

If you remain in healthiness and prepared to undergo a clinical examination, you could get typical life insurance policy at a much reduced price. Guaranteed issue life insurance policy is commonly unnecessary for those healthy and can pass a medical examination. Due to the fact that there's no clinical underwriting, even those in good wellness pay the exact same premiums as those with health issues.

Provided the lower insurance coverage amounts and greater premiums, ensured problem life insurance coverage might not be the very best choice for long-lasting financial planning. It's frequently a lot more fit for covering last expenditures rather than replacing revenue or significant financial obligations. Some ensured concern life insurance plans have age limitations, usually limiting candidates to a details age variety, such as 50 to 80.

However, assured concern life insurance policy features greater premium costs contrasted to medically underwritten policies, however rates can vary substantially depending on elements like:: Different insurer have different pricing versions and may provide various rates.: Older applicants will certainly pay higher premiums.: Women usually have lower rates than guys of the same age.

: The survivor benefit amount affects premiums. A $25,000 plan costs much less than a $50,000 policy.: Paying premiums month-to-month prices more general than quarterly or yearly payments.: Entire life costs are greater total than term life insurance coverage plans. While the ensured problem does come at a price, it offers important protection to those who might not get typically underwritten plans.

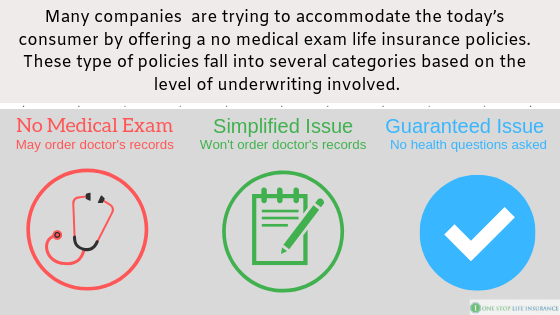

Surefire issue life insurance policy and streamlined concern life insurance are both kinds of life insurance policy that do not require a medical exam. However, there are some essential differences between the 2 kinds of policies. is a kind of life insurance policy that does not need any kind of wellness concerns to be answered.

Getting The Term Life Insurance – Get A Quote To Work

Guaranteed-issue life insurance coverage policies generally have greater costs and lower fatality advantages than standard life insurance policies. is a kind of life insurance that does require some health questions to be answered. The health concerns are usually less comprehensive than those requested for standard life insurance policy plans. This means that simplified problem life insurance coverage policies may be available to people with some health and wellness concerns.

Today, underwriters can analyze your information rapidly and concern a coverage choice. In some cases, you could even have the ability to get instantaneous coverage. Instantaneous life insurance coverage is protection you can get an instant solution on. Your plan will certainly start as quickly as your application is approved, meaning the entire process can be performed in much less than half an hour.

Instant coverage only applies to call policies with accelerated underwriting. Second, you'll need to be in great wellness to certify. Lots of internet sites are appealing instant coverage that starts today, however that does not mean every applicant will qualify. Typically, customers will certainly send an application believing it's for instantaneous protection, only to be met a message they require to take a medical examination.

The same info was then utilized to accept or refute your application. When you apply for a sped up life insurance policy your data is assessed immediately.

You'll after that get immediate approval, immediate denial, or see you need to take a medical exam. You might require to take a medical exam if your application or the data drew about you expose any kind of wellness problems or worries. There are several alternatives for instant life insurance policy. It is necessary to note that while several conventional life insurance coverage business offer sped up underwriting with rapid approval, you might need to go via a representative to apply.

Getting My Guaranteed Issue Life Insurance To Work

The business listed below deal totally on-line, straightforward alternatives. The firm provides flexible, instantaneous policies to people in between 18 and 60. Ladder plans permit you to make changes to your insurance coverage over the life of your policy if your demands transform.

The company provides plans to applications between 21 and 55 for a ten-year term, and between 21 and 45 for a 20-year term. Values plans are backed by Legal and General America.

Simply like Ladder, you might require to take a medical exam when you use for protection with Principles. Unlike Ladder, your Ethos plan will not begin right away if you require an exam.

In other situations, you'll require to provide more details or take a medical exam. Right here is a rate contrast of insant life insurance coverage for a 50 year old man in excellent wellness.

The majority of people start the life insurance policy buying plan by getting a quote. You can get quotes by getting in some fundamental information online like your age, gender, and general health condition. You can after that pick a firm and change your strategy. As an example, allow's say you obtained a quote for $50 a month for a $500,000, 20-year policy.

Higher advantage amounts and longer terms will certainly raise your life insurance policy prices, while reduced advantage amounts and much shorter terms will reduce them. You can set the precise protection you're getting and after that begin your application. A life insurance application will certainly ask you for a great deal of details. You'll need to provide your health and wellness history and your household health history.

About Instant Life Insurance Coverage With No Hassle

It is essential to be 100% honest on your application. If the firm discovers you didn't reveal info, your policy might be refuted. The decline can be mirrored in your insurance policy rating, making it tougher to get coverage in the future. Once you submit your application, the underwriting algorithm will analyze your information and draw information to come to an instantaneous choice.

A simplified underwriting policy will ask you comprehensive concerns about your case history and current medical care during your application. An instantaneous concern policy will do the very same, however with the difference in underwriting you can get an immediate choice. There are several differences in between surefire problem and instant life insurance policy.

Second, the insurance coverage amounts are reduced, but the costs are commonly greater. And also, guaranteed problem plans aren't able to be utilized during the waiting duration. This means you can not access the complete survivor benefit amount for a set amount of time. For most policies, the waiting period is two years.

If you're in great health and wellness and can qualify, an instantaneous problem plan will certainly enable you to get coverage with no examination and no waiting duration. In that situation, a streamlined problem plan with no examination might be best for you.

Little Known Facts About Best Cheap No-exam Life Insurance For Term & Whole Life.

Simplified concern plans will take a few days, while instant plans are, as the name suggests, instant. Buying an instantaneous plan can be a rapid and very easy process, but there are a few points you ought to watch out for. Before you hit that acquisition button ensure that: You're purchasing a term life policy and not an accidental death plan.

They don't offer insurance coverage for illness. Some companies will issue you an accidental fatality policy immediately yet require you to take a test for a term life plan.

Your agent has responded to all your inquiries. Similar to internet sites, some representatives stress they can get you covered today without explaining or offering you the info you require.

{kind=link}

Table of Contents

Latest Posts

The Ultimate Guide To Can I Get Life Insurance Without A Medical Exam?

Rumored Buzz on Best No-exam Life Insurance Companies (2025)

Some Known Incorrect Statements About Best No-exam Life Insurance Companies Of 2024

More

Latest Posts

The Ultimate Guide To Can I Get Life Insurance Without A Medical Exam?

Rumored Buzz on Best No-exam Life Insurance Companies (2025)

Some Known Incorrect Statements About Best No-exam Life Insurance Companies Of 2024